SNAP OUT OF IT Part 1 | Part 2 | Part 3 | Part 4 | Part 5

“…banking establishments are more dangerous

than standing armies…”

Thomas Jefferson,

letter to John Taylor, May 28, 1816

If you’ve already been suckered into building up massive debts—

Oh, are you going to hate this post.

How People with Good Intentions Enslave You to Student Loans

Here’s how people with good intentions can harm you, and never take responsibility for it.

Step 1: They persuade politicians to provide student loans for you people who want to attend college without having to work at a real job at the same time.

(Where you learn practical skills when your academic skills won’t get you a job.)

Step 2: College administrators accept students with government loans because that means more money for the colleges.

Step 3: College administrators begin jacking up tuitions, because more students with student loans provide more money to attend college.

Since the money is borrowed from the government, students have no sense of the amount of taxpayer work that had to go into generating that money. And they assume college administrators have their best interests in mind, not lining their own pockets.

Step 4: The salaries of college administrators mysteriously go up, and they create more departments and programs that don’t build practical skills for private-sector jobs in business and STEM skills (science, technology, engineering, math).

Step 5: Loan-burdened students who get non-STEM degrees (humanities, social justice, law degrees, art history, and anything with the label studies) find themselves seeking jobs that require donations or taxpayer funding, such as government jobs, non-profit organizations, teaching jobs, and academic jobs.

Step 6: Loan-burdened students don’t buy homes and often live with their parents well into their twenties or thirties. Parents can’t bring themselves to kick their kids out into the world to learn from their bad choices.

And the students don’t feel comfortable getting married and having kids. In fact, they often feel too embarrassed to have a real relationship while living at home.

Step 7: Loan-burdened students get angry with the government and societal injustice, because that’s easier than admitting that their lives suck because they made bad choices and got suckered. By the college that promised them so much.

Step 8: Loan-burdened students live a drab, wretched life. And blame life for being unfair.

(And thinking that the government was good in giving—uh, I mean loaning—them the money.)

Sadly, students are no longer taught TANSTAAFL like in the old days. I wonder why it’s no longer taught?

There Ain’t No Such Thing As A Free Lunch

How Banks with Greedy Intentions Enslave You

Think about it. You have some money. Money you worked hard for. Someone else has something to sell that you want to buy. Let’s say, new clothes.

You give them money and they give you the new clothes. Simple, right? It’s a win-win.

But there are people off to the side who look at the transactions you make and think, “How can I talk that young person into paying more for those clothes so that I can get some of that money—without having to work for it?

Here’s how they do it and do it in such a way that you have to give them more and more money, money they didn’t have to work for. It’s a lose-win-win, with you being the loser.

Here’s how it works:

Step 1: Hey, young person who doesn’t have much experience at life. Don’t have enough money to get what you want right now?

Well, why be frustrated and wait until you have the money? We have a way of helping you get what you want.

Step 2: We trust you! We are willing to give you this special thing every adult needs: CREDIT.

Yes, that’s right, you can get a credit card. Oh, joy!

(We don’t want you to think about it as a DEBT card, because, you know, credit is such a better word. It means we trust you. Debt is such a terrible word. So don’t think of it as going into debt.)

Side Note: Why are con artists called con artists? The “con” doesn’t stand for “convict.” It stands for “confidence.”

No, it doesn’t mean the con artist gets you to have confidence in the con artist. It’s exactly the opposite.

The confidence artist shows

how they have confidence in you.

They show their trust in you.

They make you feel empowered by their trust. Then they pick your pocket, all while you’re thinking it’s all your fault.

By the way, have you noticed how many institutions that want to enslave you to debt are called Trusts? First National Bank and Trust. American Trust & Savings Bank. Trust Federal Credit Union.

It used to be cathedrals that were the biggest buildings in a city. Now it’s financial institutions.

Side-Side-Note: Why are insurance companies so rich? Because most of what you fear never happens.

Step 3: You buy things on credit.

Step 4: You get your first bill.

You can afford the minimum payment, so no problem. The interest charge is small, even though the rate may be over 20%. You begin charging even more, getting close to reaching the limit.

Side-Side-Side Note: In previous centuries, the maximum interest rate for money lending was about 3%. And even then, money lenders charging such a high rate were beaten up and hanged.

So why over 20%? Well, someone has to pay for all those charges made on stolen credit cards or uncollected debts due to non-payment and bankruptcy.

Step 5: You think about paying more than the minimum payment, but that money could be spent on other things. So you end up maxing out your credit card.

Step 6: If you have a history of making your minimum payments (at high interest rates), the credit card company shows its confidence in you by raising your credit limit.

Step 7: You spend more money, get into more debt, and pretty soon, you realize that your minimum payments barely cover the interest payments. You can’t charge anything anymore.

Step 8: Your life sucks.

If you ever consider buying a home, there will be a couple of shocks that will come to you. Shocks that your lender will not want you to know. Especially if you take out a 30-year loan.

- In your first few years, your payments will be divided up this way: Out of every $100, $99 goes to the lender in interest, and only $1 gets applied to pay down the amount you actually borrowed.

Yeah, that sucks.

- The lender will do everything possible not to tell you the total amount you would pay for your, say, $200,000 home. Because it will be over a million dollars. Higher priced homes? Millions of dollars.

And sadly, you never really get to own your home. Practically speaking, you’re still a renter.

Remember, owners own a thing without obligation to anyone. No one can take away what you genuinely own. Anyone who does is a thief.

Renters can be kicked out for non-payment. Because they have landlords.

Homeowners don’t have landlords, right? But wait. You forget that they have to pay property taxes, a kind of annual rent. The state and federal governments are their landlords.

If you think you own your home, try not paying your property taxes and see what your very real landlords do to you.

How Governments Con You

But governments are good! They make things fair! We can trust them!

Yeah, riiiiiight.

This is such a big story that the full version is told in my book Money and Wealth.

Here’s a little, tiny piece of that book.

A History of U.S. Money

That paper money has some advantages is admitted. But that its abuses also are inevitable, and, by breaking up the measure of value, makes a lottery of all private property, cannot be denied. Shall we ever be able to put a constitutional veto on it?

Thomas Jefferson,

letter to Dr. Josephus B. Stuart, May 10, 1817

As you read this post, please:

Don’t freak out!

Ripping away the pretty mask of government financial actions often causes people to act rashly: protesting taxes, going on anti-government campaigns, making emotional investments.

The history of U.S. money reflects practices

that governments have engaged in

for thousands of years.

All governments today have done what the U.S. government has done.

You’ve heard that power corrupts, and absolute power corrupts absolutely. Manipulating the definitions of money is standard practice for power brokers, both in government and in financial institutions.

I propose that, by going through this history, you will be better informed to make financial decisions. If you freak out instead, you take on unnecessary risks.

Okay. Let’s begin…

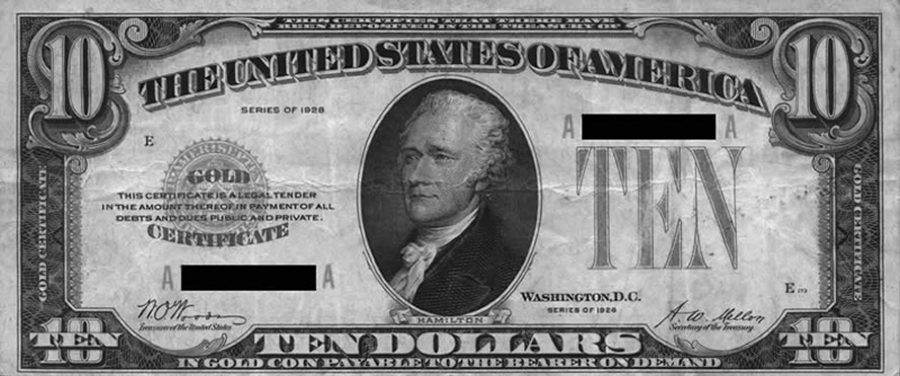

Here is an example of legitimate paper money, a U.S. Gold Certificate, issued 1863-1934. Pay attention to its exact legal language:

THIS CERTIFIES THAT THERE HAVE

BEEN DEPOSITED IN THE TREASURY OF

THE UNITED STATES OF AMERICA

TEN DOLLARS

IN GOLD PAYABLE TO THE BEARER ON DEMAND

Notice that on the left between the words “Gold” and “Certificate” is the statement: “This certificate is a legal tender in the amount thereof in payment of all debts and dues public and private.”

This note is an IOU. It is not money. It is a symbolic representation of real money, gold, on deposit in the U.S. treasury. The bearer of this note can, ON DEMAND, trade it in for gold.

The same is true of Silver Certificates, issued 1886-1963.

THIS CERTIFIES THAT THERE HAVE

BEEN DEPOSITED IN THE TREASURY OF

THE UNITED STATES OF AMERICA

ONE DOLLAR

IN SILVER PAYABLE TO THE BEARER ON DEMAND

Notice how the language has been simplified to the left of the president:

THIS CERTIFICATE IS LEGAL TENDER

FOR ALL DEBTS PUBLIC AND PRIVATE

One thing should be obvious about both of these certificates: Neither is gold or silver.

But a couple of things are not so obvious:

Notice that the gold certificate will pay ten dollars in gold. And the silver certificate will pay one dollar in silver. These certificates are not dollars.

Remember from previous chapters when we talked about measuring gold in ounces. Well gold and silver were also measured in dollars.

Think about it this way: Suppose someone came up to you and said, “Do you want to buy a gallon?”

You would be confused.

Why?

Because that question makes no sense.

You would rightly ask, “A gallon of what? A gallon of milk? A gallon of gas?”

A unit of measurement has no meaning

except when it measures something.

Notice that the gold and silver certificates measure something: ten dollars in gold coin, one dollar in silver.

In earlier days, if one person asked another, “Would you like a dollar?” the person asked would answer, “A dollar of what? Gold? Silver?”

Definitions of words are important. When you change the definition, you change the picture people hold in their minds.

Therefore, manipulating definitions

is one method of a kind of mind control.

In 1913 the U.S. Congress passed the Federal Reserve Act. Soon after, the Federal Reserve began issuing Federal Reserve Notes (FRN).

And the language began a subtle transformation. The first FRNs stated that they were redeemable in gold on demand (see the text to the left of the president).

But do you notice a subtle change in the language of the note?

First, in the text to the left, there is a new phrase. The note is redeemable “in gold or lawful money at any Federal Reserve Bank.”

So the Federal Reserve can have something other than gold as lawful money?

Perhaps they mean silver, or something else. But there is another subtle shift in the language.

Can you see it?

Look at the text above and below the president.

FEDERAL RESERVE NOTE

WILL PAY TO THE BEARER ON DEMAND

FIVE DOLLARS

See the shift? Even though the note elsewhere states the note is redeemable in gold or lawful money, the note now states the unit of measurement (five dollars) disconnected from gold or lawful money.

Isn’t that interesting?

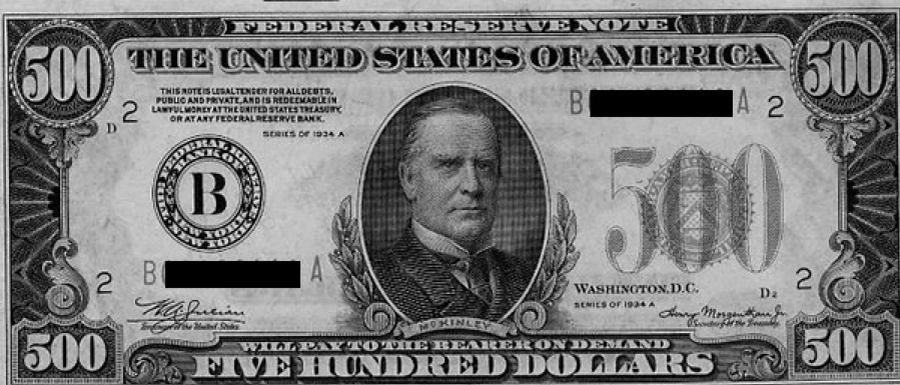

The Federal Reserve issued the FRN pictured above in 1928. Six years later it issued the FRN pictured below.

See something missing?

The statement to the left of the president says, “This note is legal tender for all debts public and private and is redeemable in lawful money at the United States Treasury or at any Federal Reserve Bank.”

The note has been completely

disconnected from gold.

You may recall that President Franklin Delano Roosevelt made the ownership of gold illegal and withdrew it from circulation.

Now people were expected to redeem these notes for silver or whatever the government deemed as lawful money.

Not a problem, right?

Let’s see…

In 1963 the Federal Reserve Bank took the next step in transforming (redefining) U.S. money. They began withdrawing silver from the economy that year. They also issued a new FRN.

To the left of the president is the statement, “This note is legal tender for all debts public and private.”

Above and below the president was this text:

FEDERAL RESERVE NOTE

THE UNITED STATES OF AMERICA

ONE DOLLAR

Notice anything missing?

No mention of gold, silver, lawful money, or anything making this note redeemable. Before 1963 all U.S. paper money measured gold, silver, and lawful money in dollars—a dollar in gold, a dollar in silver, a dollar in lawful money.

But in 1963 that all changed.

Citizens and foreign governments were expected to forget redeeming notes. Instead the note proclaims itself as one or more dollars.

In 1963 when the first FRNs were issued about the time of President Kennedy’s assassination, a mother could go into a bank with a pile of silver dollars and deposit them. Then, remembering, she turns around and says, placing an FRN on the counter, “I forgot. It’s my daughter’s birthday, and I want to give her a silver dollar.”

And the bank teller would respond, “We’re sorry, but all silver dollars are being withdrawn and replaced with FRNs, because, you know, there is just not enough silver to go around, and it makes more economic sense to transition to a paper money, which are just as good as any dollar, you see.”

All the new coins were made, not with silver, but with nickel and copper.

By 1971, the U.S. government had printed up so much “money” that France and other countries began to distrust its value. They began trading in U.S. “dollars” for gold in the U.S. Treasury. To stop this run on gold, President Nixon ended the “Gold Standard.”

This action simply meant that FRNs were no longer redeemable. The government keeps the gold and silver, and everyone else gets paper.

That’s a fair exchange for a working economy, right?

Today’s currency is not money.

It has no intrinsic value.

And as the government via the Federal Reserve prints up more money (electronically these days), the value of that money decreases. But real gold and silver preserves value.

In 1971, gold was valued at $35 per ounce. As of this writing (summer 2013) gold is valued at $1,400 per ounce.

In the early 1960s, a gallon of gas could be purchased in some areas of the country for a silver quarter. Today that old, silver quarter can still buy you a gallon of gas in many areas of the country. Because the silver in it makes it real money.

Gold and silver tend to preserve their value. Even though more dollars are needed to buy an ounce of gold, that ounce of gold or silver still buys the same value of things it used to buy.

In sum, governments that control money and currency will find ways to spend what they don’t have. Since citizens do not generally understand the nature of coin, currency, and circulation, nor do they like ever rising taxes, governments find ways of indirectly taxing them through inflation.

Money can’t be created out of thin air, but currency can. And the result of more paper chasing goods and services is a rise in the cost of goods and services.

Side Notes

Note 1

By the way, have you ever wondered who got all the gold and silver that was withdrawn from circulation?

Note 2

Remember the “mill marks” that were engraved on the edges of coins to stop people from shaving the coins and melting down the shavings?

Gold and silver coins had those mill marks, but nickel and copper coins did not. No one shaves base metal coins and melts down the shavings for their value.

But now that dimes, quarters, half-dollars, and dollars are made of nickel and copper, why keep the mill marks?

Perhaps to keep up the illusion that they are money?

Okay. Enough. You now need a humor break, right?

![]()

Albert Einstein, the great genius physicist, dies and goes to heaven only to be informed that his room is not yet ready. The doorman tells him, “I hope you will not mind waiting in a dormitory. We are very sorry, but you will have to share the room with others.”

Einstein says that this is no problem at all and that there is no need to make such a great fuss. So the doorman leads him to the dorm. They enter and Albert is introduced to all of the present inhabitants. “See, Here is your first roommate. He has an IQ of 180!”

“That’s wonderful!” says Albert. “We can discuss mathematics!”

“And here is your second roommate. His IQ is 150!”

“That’s wonderful!” says Albert. “We can discuss physics!”

“And here is your third roommate. His IQ is 100!”

“That’s wonderful! We can discuss the latest plays at the theater!”

Just then another man moves out to capture Albert’s hand and shake it. “I’m your last roommate and I’m sorry, but my IQ is only 80.”

Albert smiles and says, “So, where do you think interest rates are headed?”

The only advice I have to people with massive debts? Tighten your belt and make you’re your financial decisions ones that reduce and eventually eliminate debt.

![]()

You want to be on the asset side of life for a change.

Oh, and never spend money on lottery tickets. You have a better chance of being hit by lightning.

Remember…

It doesn’t matter what happens to you.

What matters is how you respond.

Only you are in charge of your responses. Take back ownership and watch what changes.

Pingback: Get Toxic, Angry People Out of Your Life | Mark Andre Alexander

Pingback: Taking Charge of Your Imagination | Mark Andre Alexander

Pingback: How to Quit Smoking and Other Imagination Exercises | Mark Andre Alexander

Pingback: Children, Adults, and Rites of Passage | Mark Andre Alexander

Pingback: Individuals and Groups | Mark Andre Alexander

Pingback: Colonialism and Home Rule | Mark Andre Alexander

Pingback: The Truth about Happiness | Mark Andre Alexander

Pingback: Afterword | Mark Andre Alexander